EU Meat Production Set to Fall for 2021

2nd November 2020

Peter Duggan, Meat Division, Bord Bia – The Irish Food Board

The latest short term outlook from the EU Commission for agricultural products shows some downward pressure on meat production with the exception of poultry meat. This overall picture reflects the impact of Covid-19 and some fall off in producer confidence across certain meat categories, as a result of the current pandemic and the threat of animal diseases spreading to Western Europe.

Pigmeat

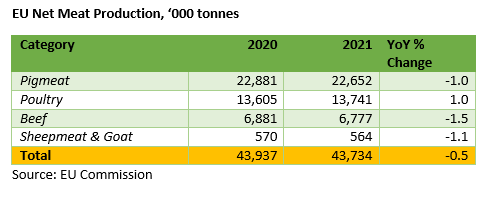

Pigmeat production is expected to fall by 1% to 22.7 million tonnes during 2021 reflecting the uncertainty the sector faces following the discovery of African Swine Fever (ASF) from wild boars in the Brandenburg region of German in early September. This development is significant as Germany is one of the leading EU pigmeat suppliers, and exports 27% and 41% of pigmeat and offals, respectively to China alone. As a result, German pig producer prices have fallen sharply in recent weeks as pigmeat exports to key partner markets such as China, Japan and South Korea were banned. If German suppliers face being blocked from supplying these incredibly important markets for a prolonged period, this will put further pressure on German suppliers to reduce production and also live piglet imports from Denmark. This is likely to have a significant impact on Danish production as well, as they rely on live piglet exports as they do not have finishing capacity within their own market due to strict environmental controls that increase production costs.

Beef

For beef, production is expected to fall by almost 2% to 6.8 million tonnes during 2021 reflecting some noticeable decline in the EU herd based on the latest June livestock survey for France, Germany and Ireland. EU beef exports are expected to fall by around 4% on the back of tighter domestic supplies. Due to the impact of Covid-19, consumption is expected to be around 1% lower as the foodservice channel will remain affected.

Poultry

The growth in poultry meat production is expected to continue into 2021 reflecting the shift in demand from other meats to poultry as European economies and consumers struggle in response to Covid-19. Poultry output has benefitted from strong investment in recent years around Europe, and Poland in particular. This trend is likely to continue but at a slower rate over the short to medium term as companies in numerous countries adapt to fragile consumer sentiment and poultry related diseases such as Avian Influenza.