Global pig sector faces a variety of different headwinds in different regions

John Tobin, Data and Market Intelligence Specialist

The recent GIRA Meat Club was held in Geneva in December 2023 and provided conference attendees an in-depth analysis of the challenges and opportunities facing the animal protein sector on a global and regional level with associated five year forecasts in terms of production and consumption. The below article provides a brief overview of some the key headwinds affecting the pork sector in China, the US and Europe

The recent GIRA Meat Club was held in Geneva in December 2023 and provided conference attendees an in-depth analysis of the challenges and opportunities facing the animal protein sector on a global and regional level with associated five year forecasts in terms of production and consumption. The below article provides a brief overview of some the key headwinds affecting the pork sector in China, the US and Europe

Chinese pork outlook

In terms of the outlook for pork in China. Overall, it was highlighted how the reopening of the Chinese market following the abandonment of its Zero Covid-19 policy that overall demand stalled and represented one of the first times the Chinese market did not recover from such an event rapidly. It is expected consumption not to recover to pre African Swine Fever (ASF) levels with consumption in 2028 forecasted to be down 10% when compared with consumption in 2018. The primary reason for this decline in consumption is attributed to the expansion of alternative protein offerings. In addition, similar to other pork producing countries the sector faces profitability challenges, with one of the primary solutions to this believed to be that capacity must be reduced. However, there’s a general reluctance amongst the main producers to make such a cut in production currently. It was also noted how in recent years the small to mid-size holdings that were previously the primary source of volatility have now been replaced by well financed tech oriented new entrants.

Contraction in EU Pork Production

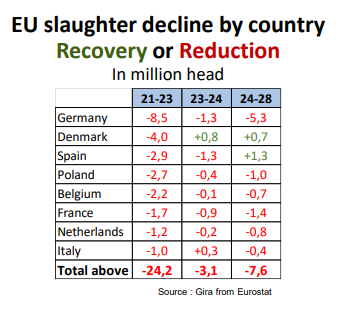

Within Europe, unfortunately the narrative was quite negative despite good producer margins throughout 2023, attendees were informed that a reorganization has commenced in the slaughter and further processing sector with the closure of some plants now unavoidable due to the decline in the overall pig herd in Europe. To add context to this, EU-27 pig slaughterings were c.250 million head in 2021 and by the end of 2023, it is estimated that 28 million fewer pigs will be slaughtered. For instance, production in Germany is estimated to be down by 9% in 2023. The challenges in Germany are due to less live piglet imports, increased costs associated with ASF export barriers and “5*d” believed to be not delivering for the industry (an initiative that pays more for pigs that are born and raised in Germany). GIRA forecasts out to 2028 suggest a further contraction of eight million less pigs available for slaughter, which would mean the EU pig sector, could contract by almost 15% by 2028. As a result, it was suggested that this may force some producers on the continent to exit the sector too, due to increased transport costs associated with delivering pigs to plants further away. However, it was noted that this could present some opportunities for production to expand for producers located close to plants that remain open.

Within Europe, unfortunately the narrative was quite negative despite good producer margins throughout 2023, attendees were informed that a reorganization has commenced in the slaughter and further processing sector with the closure of some plants now unavoidable due to the decline in the overall pig herd in Europe. To add context to this, EU-27 pig slaughterings were c.250 million head in 2021 and by the end of 2023, it is estimated that 28 million fewer pigs will be slaughtered. For instance, production in Germany is estimated to be down by 9% in 2023. The challenges in Germany are due to less live piglet imports, increased costs associated with ASF export barriers and “5*d” believed to be not delivering for the industry (an initiative that pays more for pigs that are born and raised in Germany). GIRA forecasts out to 2028 suggest a further contraction of eight million less pigs available for slaughter, which would mean the EU pig sector, could contract by almost 15% by 2028. As a result, it was suggested that this may force some producers on the continent to exit the sector too, due to increased transport costs associated with delivering pigs to plants further away. However, it was noted that this could present some opportunities for production to expand for producers located close to plants that remain open.

New production standards in the US

Looking to the US market, similar to China, overproduction and losses at production level were the dominant themes, though exports of US product were boosted by the supply contraction in the EU. One of the main developments in the US was the introduction of Prop 12. Prop 12 is a new requirement that stipulates minimum space requirements for egg laying hens, breeding pigs and calves raised for veal. With the implication that only product that is compliant with this standard permitted to be sold in the state of California. With regards, to pork consumption California is estimated to account for 14% of overall US pork consumption so the state is a significant market for pork. However, uncertainty lies around just how much pork output is deemed to be meeting this standard in the US with the expectation amongst attendees with knowledge on this, that the figure was quite low in addition to demand from premium retailers elsewhere in the US for product meeting this specification. Of greater concern to the industry though is the additional cost this is placing on producers and processors alike at a time when the sector is generating losses and also of the additional cost this places on consumers, some of whom have restricted budgets with regards to food expenditure. Separately in Massachusetts a new proposal called Massachusetts Question 3 is yet to be implemented. These developments do raise concerns of viability for producers and processors in meeting a proliferation of standards in the US, in addition to concerns around enforcement and affordability for lower income consumers.

In conclusion, it looks like the global pork industry is facing a number of different challenges in different regions. From an EU perspective 2024, looks to be a positive year for producer with improved margins. However, overall pork consumption per capita in the EU is expected to decline in the medium term with France and Germany expected to be disproportionally affected relative to other member states. However, despite this somewhat negative sentiment it is believed that those producers close to plants that remain open may have opportunities to expand. Outside of the EU, it looks like pork exports to markets such as China may be challenged given the oversupply situation. For clients interested in learning more about GIRA’s latest findings or insights affecting the global pork sector, please email: thethinkinghouse@BordBia.IE.

References:

Cadudal, F. (2023). World Synthesis - Pork. Geneva: GIRA.

Claxton, R. (2023). USA Pork. Geneva: GIRA.

Herzfelder, R. (2023). China’s Pork Sector. Geneva: GIRA.

Van Ferneij, J.P. (2023). EU Pigmeat - Unprecedented Production Reduction. Geneva: GIRA.