The Impact of Coronavirus on UK Shopper and Consumer Behaviour – Part 3

28th September 2020

Kerri Murphy, UK Market, Bord Bia - The Irish Food Board

The Him MCA UK recovery report examines the state of play for the UK food industry and looks at the business implications of the coronavirus pandemic, as well as the key learnings to help food and drinks businesses navigate this new landscape and the changing consumer attitudes that come with it. The change in how we live and work and the ‘new norms’ we are becoming secondary to have an impact on how consumers shop and socialise and we can only expect that this will have long-lasting impacts on the industry. This FoodAlert, the final in a three-part series, is built on insight from MCA’s UK Recovery Report and considers the future scenarios for the UK retail and foodservice landscape and what this means for Irish suppliers in the market.

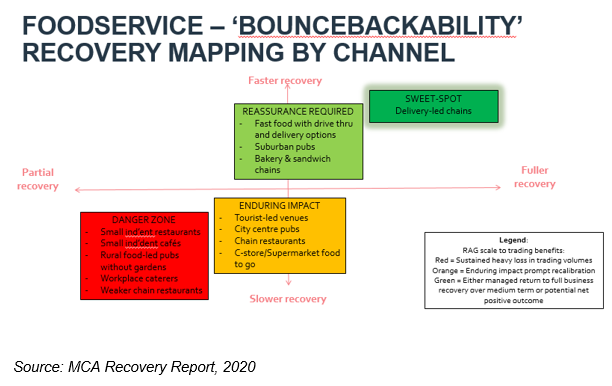

It is be no surprise to say that the UK foodservice landscape will be permanently changed due to the impact of coronavirus. Recovery of the sub-channels will be varied, depending on several factors such as location, reliance on tourism and delivery capabilities. There is a threat to smaller operators due to cashflow and lack of delivery capabilities. As recovery will be heavily dependent on-site location, those reliant on office workers, tourists and older-age consumers will see a slower recovery. However, MCA forecast that operators with established loyalty, stronger delivery and drive-thru revenues, lower ticket spends and in suburban locations will be more insulated while delivery chains will thrive.

Looking forward we can expect some operator closures and high levels of promotional activity across the board to lure customers and retain them aided by government support initiatives such as the Eat Out to Help Out (EOTHO) scheme. EOTHO in the UK led to more than 100 million meals being claimed by the scheme. Food sales from CGA’s pool of 7,000 foodservice outlets showed food sales on Monday 7 September were down by 63% on the previous Monday—the last day of Eat Out to Help Out. However, sales were still up by 27% on the equivalent day in 2019 as some operators continue to fund early-week discounts, an illustration.

Full market recovery in the foodservice market, with a return to economic growth, much strengthened consumer confidence and an end to any lingering coronavirus re-emergence risks is estimated by MCA to take around 3-5 years to come to fruition. The most likely scenario in the short term is a volume-rich market, with faltering consumer confidence amid ongoing concerns around viral infections and the job market, resulting in declining spending power and out of home influence and more focus on local community support. This will result in more in-home occasions, however there will be scrutiny about spend making low prices and promotions key to budget conscious shoppers.

Grocery retailers that saw stronger virus-related trading uplifts are expected to retain some sustained benefits going forward. However, city centre-based retailers, those without delivery operations and those more dependent on commuter/worker footfall for food to go sales, are likely to be less well placed. The discounters are likely to benefit due to the focus on value as we inevitably go into recession. This is already being seen in the market with Tesco mov

Implications for Irish suppliers

- Hygiene will remain a priority, suppliers need to consider the hygiene of their products and packaging in retail. However, retailers are returning focus to plastic reduction targets so suppliers will need to consider how to balance consumer hygiene concerns with retailer sustainability pledges.

- Reduced consumer confidence will lead to restricted spending and a higher importance placed on value. Consider how you can increase the perceived value of your products to appeal to this need.

- Delivery and local stores will continue to win, consider distribution to ensure regional coverage. This will be increasingly important as local lockdown measures may potentially be implemented across the UK.

- Values-led agenda will win – consumers favour responsible consumption and those brands they trust and who do the right thing. Consider how you communicate your brand values to UK consumers.

- Recovery for the foodservice channel will be slow. While government initiatives such as the EOTHO scheme provide a temporary boost they also drive footfall through low-prices. Foodservice will remain value and price driven in the short to medium term.

For more information on Bord Bia’s Covid-19 Response, visit the Bord Bia Covid-19 Hub by clicking here.

Source: MCA Recovery Report, 2020, Bord Bia Consumer Lifestyle Trends