Brexit Trade Agreements and Beef in the UK

Sean Deane – UK Market Specialist Meat & Organics

Australia and New Zealand can now export more beef to the UK market due to Brexit. This article examines the impact of this due to the new Free Trade Agreements (FTAs) signed by the UK with these two countries. This article is based on a presentation from Gira at the Inaugural Irish Beef UK Market Seminar that took place in London, February 2024.

UK Import Market

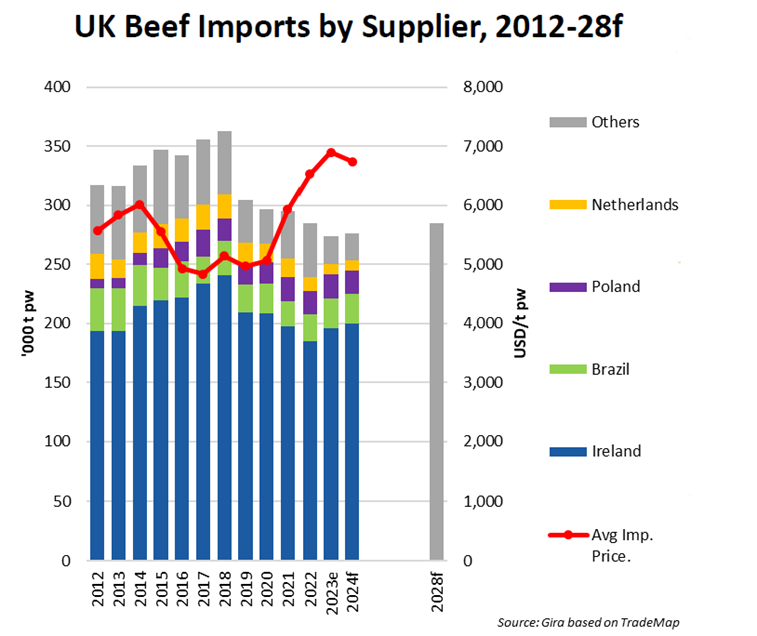

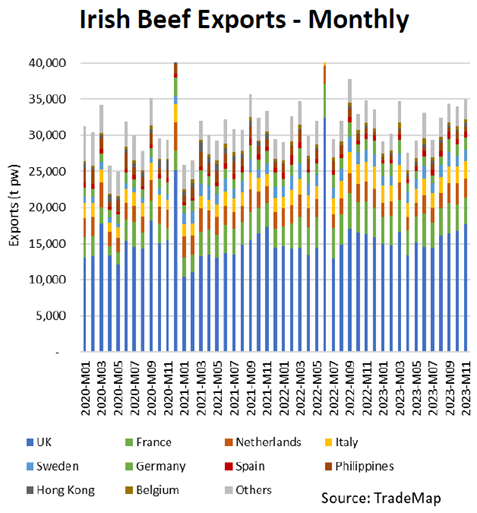

The UK currently imports ~300 thousand tonnes per year, with raw beef (mainly hindquarter cuts & mince) dominating import values.

The UK has a long-term reliance on the Irish beef sector with ~75% of UK beef imports from Ireland and nearly 50% of beef produced in Ireland destined for the UK (approximately 23% of consumption).

Along with this, Irish beef has a major presence at retail due to it being viewed as interchangeable with British beef by retailers & consumers.

There is currently a small volume of non-EU beef from Brazil and there's also a Tariff Rate Quota (TRQ) for seven thousand tonnes of hormone free beef under the Hilton quota.

*pw refers to product weight

Free Trade Agreements

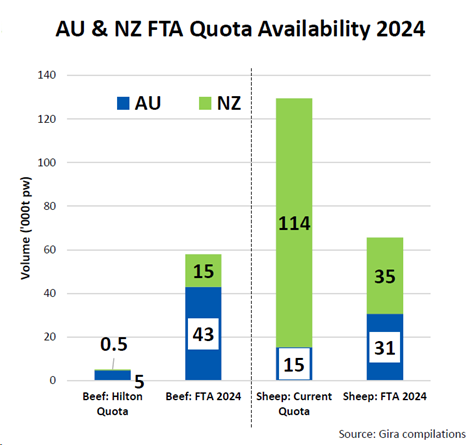

Post Brexit, the UK signed FTAs with Australia (AU) and New Zealand (NZ). According to Gira, these are not focussed on protecting UK agriculture. From year one to year ten (2023 –2033) the quota for beef will rise from 35,000 tonnes to 110,000 tonnes. Post the transition period imports of beef from AU and NZ will no longer be subject to tariffs.

Australian Beef Production & Exports

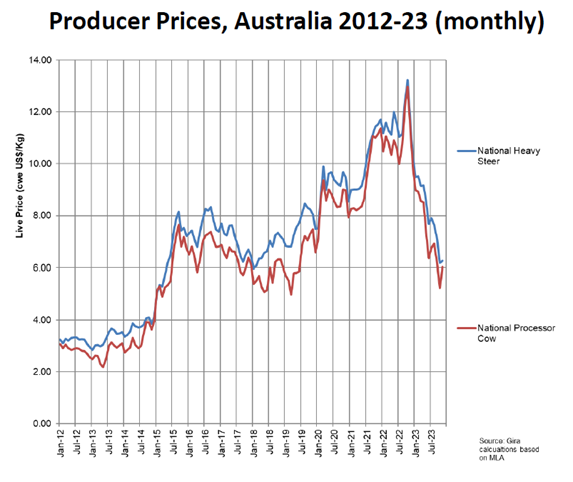

In 2023 there was a dramatic price crash in Australia with live prices averaging -41% below 2022 levels. Processor margins remained strongly positive since April 2023 reaching a record high in September.

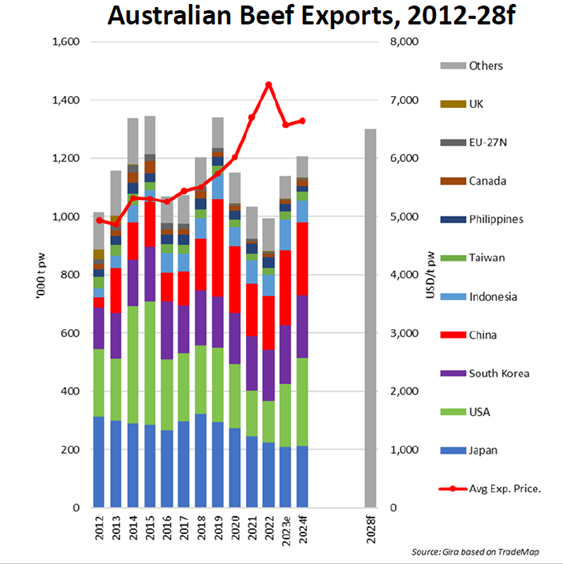

AU beef exports experienced strong volume gains throughout 2023 to most destinations USA: +48%, China: +37%, South Korea: +16%, Indonesia: +50%, Japan: -6%.

There is continued opportunity in the US as they are currently operating well below TRQ (375 thousand tonnes) along with an improvement in relations.

FTA Impact

NZ lamb has given the UK retailer a taste for value offers which may open discussions for AU beef. The focus will be AU beef as NZ has less suitable beef. AU beef (grain-fed – full carcasses) has historically worked well in UK foodservice with all cuts selling well but AU must produce these whole carcasses to EU/UK standard (hormone free). So, a long lead time is needed to scale this supply chain.

Although this may seem like a threat to Irish beef exports, in the medium to long-term, it will take time for Australian beef to build out a robust supply chain and they will still be limited by quota. To continue the strong Irish position, Irish beef must play to its key strengths, including proximity to the UK market, interconnected supply chains, consumer acceptance, sustainability credentials and trusted relationships with key partners. With all of this in mind it is likely that UK importers may use the lower AU prices as a negotiating tool, but we will not see any major changes in the short term to the UK Import market.

References:

GIRA (2024b). UK Beef Market & FTA Impact. Bord Bia.