Kantar Christmas 2023 Meat Shopper Retail Trends

Shauna Jager- International Graduate, Meat

Kantar presented their meat shopper trends for Christmas 2023 and the number of weeks leading up to it in Bord Bia at the end of February. Their analysis of the festive season unveiled a number of key themes that shaped the retail landscape and consumer behaviours during this period. This insightful article delves into these themes and other meat specific trends to note on consumers behaviour during and in the lead up to Christmas 2023.

The Kantar Meat Shopper Trends for Christmas 2023 showed an especially busy period for retailers with a record-breaking €1.4 billion spent by consumers in Irish retailers during the month of December 2023. This was a 7.8% increase (+€102.5 million) on the same period in 2022. The 7-day lead-up to Christmas, showed strong increases, particularly Friday the 22nd and Saturday the 23rd.

The key themes this Christmas in Ireland, according to Kantar were:

- Grocery Inflation, which remains prominent at 7.1%.

- Frequency was up, as the Christmas 2023 period recorded the highest number of in-store trips ever seen at 42 million (3.4 million more than 2022)

- Trading up/down, the retailer private labels are a key lever for shoppers with managing tight household budgets (but still indulging), with brands seeing a noticeable uplift in December 2023 accounting for 53% of sales.

- Sales of items on promotion was at its lowest level in five years at 30.7% (compared with 36.7% in December 2019), but vouchering had a role in influencing this.

Retailers

Each of the big five retailers battled for loyalty and offered value offers to attract shoppers. Each of these saw growth in percentage value share across the Christmas period, the largest being 11.3% for Dunnes Stores. Inflation did continue to have an impact on these value shares, with the average spend per buyer being €767 over the Christmas period, €41 more than 2022. As people ‘shopped around’ for better value, the biggest movement was to Dunnes Stores, Lidl, and Tesco in that order. With Aldi and Supervalu both losing out.

Meat categories that drove this value and volume growth across all retailers were Poultry and Beef, with a 30% volume increase in roast beef and a 10% volume increase in fresh poultry seen during the 4 weeks leading up to Christmas.

Meat Specific Trends

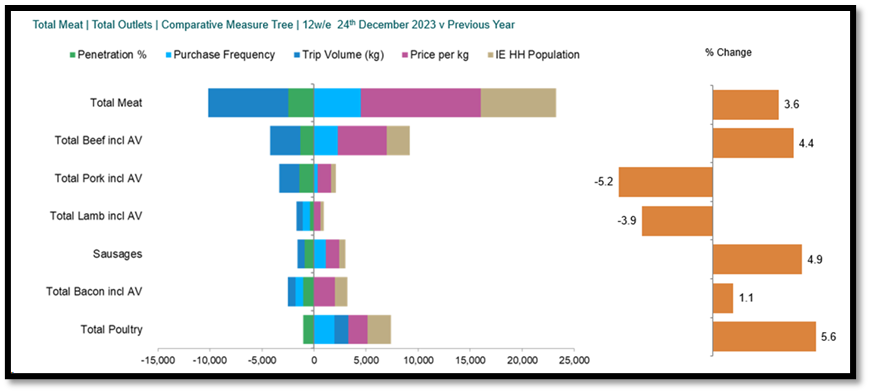

Total meat saw an increase of +3.6% in the 12 weeks running up to Christmas. Price increases being the primary driver of growth, increasing by 3.2%. Other drivers included the number of buyers and frequency, which both increased, 1.3% and 1.2% respectively.

Source: Kantar

All sectors within total meat saw increasing price and decreasing penetration in comparison to last year, poultry being the only sector to witness volume growth. This drove total growth in poultry, up to 5.6% year on year. Bacon (including added value) saw a 4.9% increase and beef saw a 4.4% increase. The most notable change over the past four years within the total meat category, is that chicken is becoming increasingly popular in the weeks leading up to Christmas seeing steady growth from 21.4% total value share in 2020 to 24.6% in December 2023. This came while the value share for beef and lamb during this same period saw decreases, from 32.5% to 31.4% and 6.1% to 4.7% respectively. Beef is still holding the largest value shareholder for the 12 weeks leading up to Christmas. Looking in volume terms, chicken holds the highest volume share consistently over the last four years, seeing increases totalling 1.7% since 2020. Beef and lamb both see a slight decline in volume terms at 0.4% and 0.9% respectively.

In the 12 weeks leading up to Christmas, shoppers moved to more expensive higher valued cuts, with beef joints seeing a strong increase. Price increases were seen across all sectors, with total pork seeing the largest percentage increase at +5.4%. The average price for lamb remained to be the most expensive across all sectors, seeing 3.3% growth year on year.

Brands vs Private Label

Within the total meat category, shoppers have spent two million less on branded products, with more standard private label brands leading the largest sales increase and more premium private label following that, seeing an increase of €2.6 million. In value terms across the sectors, beef saw the strongest jump on private label shares, at just under 6%. An overview of the various private label tiers (premium private label, standard private label, and value private label) over the last four years shows that premium private label has gained share, growing from 7.8% at Christmas 2020 to 9% in Christmas 2023.

Bacon and beef products are where shoppers were trading up, to more premium private label while this saw losses to the spend in more standard or value for money private label within bacon and poultry. Bacon seeing a €476,000 increase in value private label and poultry seeing a seven million euro increase within standard private label.

Looking at expenditure on meat across life stage demographics; young families hold the highest share of standard private label meat. Branded products over index with older dependants and retired, with older dependants holding the highest share of premium private label meat, at 9.5% followed by empty nesters and then retired. Older Dependants have the highest share across all sub sectors over indexing in lamb and bacon. The cheaper meats like poultry over index with the more price conscious Pre-Families. Older Dependants have reduced their spend across all subcategories bar poultry and bacon, whilst the Retired and 45+ Family show largest contribution increases to the meat category in the last year.

Overall, Kantar’s insight showed shoppers frequenting retailers more often, reflecting a deliberate effort by consumers to make the most out of their spending budget during the festive season. This demonstrated a strategic approach, where consumers are planning their purchases to get better value for their purchases. The inclination towards trading down to premium private label from branded products indicated an effort to keep managing budgets effectively without compromising on quality.

References:

Kantar (2024). Christmas 2023 Meat Trends with Kantar Ireland. Kantar.