Peter Duggan, Meat Division, Bord Bia - The Irish Food Board

After a year where the African Swine Fever (ASF) epidemic caused unprecedented changes to the global meat landscape. The unfolding of the Covid-19 pandemic has added an additional layer of complexity in response to the sudden change in global consumer behaviour. In particular, the foodservice channel has almost ground to a halt as a result of several ‘national lockdowns’ across the globe.

Irish meat producer prices have come under severe pressure over the past number of weeks. Beef prices are particularly sluggish as demand for premium steak cuts that would mostly be consumed in restaurants across Europe and Ireland has slowed considerably. This is further compounded where many fast food restaurants remain closed across Europe where manufacturing beef is mostly used for burgers. For pigmeat, the logistical challenges that followed the fallout of Covid-19 across Asia has impacted on trade levels. In particular, during the month of March and early April, securing reefers across Europe to supply International markets was particularly challenging.

Looking ahead to prospects for the year ahead. The global meat trade will be severely constrained by the shock to the system that has resulted from the widespread closure of businesses in the food service channel.

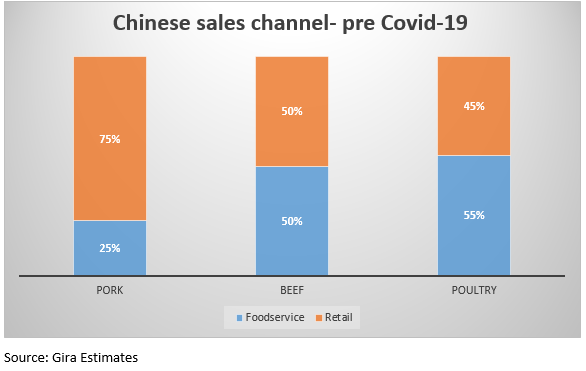

The challenge facing the beef sector is around maximising carcase value in Europe and driving demand within the retail channel across Asia as consumers remain cautious towards dining out. In China, around 50% of beef consumed is within the foodservice channel. For 2020, GIRA anticipate that Chinese beef imports will fall by 11% to 2.56 million tonnes. On the other hand, given that pork is the staple dish for most Chinese consumers, with around three quarters of total pork purchased through the retail channel. The pigmeat category is better positioned to withstand the current global turbulence, given the ongoing challenges in Asia around securing enough meat protein reflecting the impact of ASF. Chinese pigmeat production is forecast by Gira to reach around 21.75 million tonnes this year or 58% lower compared to 2018 levels. A delay in the recovery of pigmeat production in China as a result of Covid 19 is expected to leave Chinese pigmeat imports 61% higher at 3.52 million tonnes for 2020 compared to prior year levels. However, European suppliers will be challenged by more competitively priced US pork. This is due to limited meat packing capacity reflecting some plant closures from Covid 19 combined with surplus pigs has led to significant price cuts for producers in recent weeks. In addition, Gira estimate that the foodservice channel in the US accounts for almost 40% of pigmeat consumption, the collapse in this channel has resulted in pork belly demand and prices declining significantly.

Sources:

https://www.bordbia.ie/farmers-growers/prices-markets/cattle-trade-prices/

https://www.bordbia.ie/farmers-growers/prices-markets/pig-trade-prices/